America is a generous country. People with diverse backgrounds can unite for a good cause, whether to benefit their local communities or the broader world. As we enter the holiday season, now is a great time to think about your giving strategy and your contributions to the charitable organizations and causes you care most about. Not only does charitable giving benefit those in need of help, but it also can benefit you personally by giving you a sense of fulfillment.

Trends in Giving

According to Giving USA’s Annual Report on Philanthropy, individuals, endowments, foundations, and corporations gave an estimated $557.16 billion to U.S. charities in 2023.1

Affluent Americans continue to show their generosity by giving back. The 2023 Bank of America Study of Philanthropy found that 85% of wealthy households gave to charity in 2022, with the value of their average gifts rising 19% above pre-pandemic levels. Put another way, affluent American households gave $34,917 on average to charitable organizations.2

(The Bank of America study defined the affluent as households with a net worth of $1 million or more [excluding the value of their primary home] and/or an annual household income of $200,000 or more.)

Interestingly, women are the primary decision-makers in household charitable giving, while Millennials and Gen Z are emerging as critical groups in philanthropy. Four in five younger affluent households already give to charity. That said, they are more likely to give to an environmental organization than to religious/spiritual groups or those that provide basic needs or support the arts.2

Impact Is About More Than Just Money

The commitment of affluent households to their favorite charities goes beyond financial. Volunteering is on the rebound after the pandemic. In 2022, nearly 37% of affluent households volunteered their time and talents to charitable organizations and causes, a number up from 30% in 2020.2

Affluent volunteers spent an average of 135 hours with an average of two different charitable organizations in 2022, with the most common activities being helping a religious organization, collecting and distributing food, clothing, or other basic needs, and serving on an organization’s board.2

These volunteers believe their service makes a difference, with 93% of those feeling personally fulfilled by their actions. Moreover, those who volunteer are more likely to give financially to a charity than those who do not (94% and 80%, respectively), and the median gift amount by volunteers is nearly four times more than that of non-volunteers.2

Choosing a Charity to Support

With so many charities, choosing which ones to support can be challenging. By researching and preparing, you can find a charity that aligns with your values.

- Research the Charity: Use publicly available sources to understand what a charity does and who it serves. One factor to consider is the group’s transparency and accountability in financial reporting and program effectiveness. You can also get information on websites such as Charity Navigator, GuideStar, or the Better Business Bureau’s Wise Giving Alliance.

- Understand the Mission and Impact: Another factor to consider is whether the organization’s values and goals align with yours. Look for a clear and measurable impact on the community or cause they serve. Consider the scope of their programs and services.

- Your Interests and Passions: Your interests and passions can help you find a cause that resonates with you and inspires you to make a difference.

- Getting Involved May Help You Learn More: Many charities offer volunteer opportunities or ways you can participate in their events and campaigns. These opportunities can give you an even greater understanding of the charity’s impact while helping you build a deeper connection to the cause.

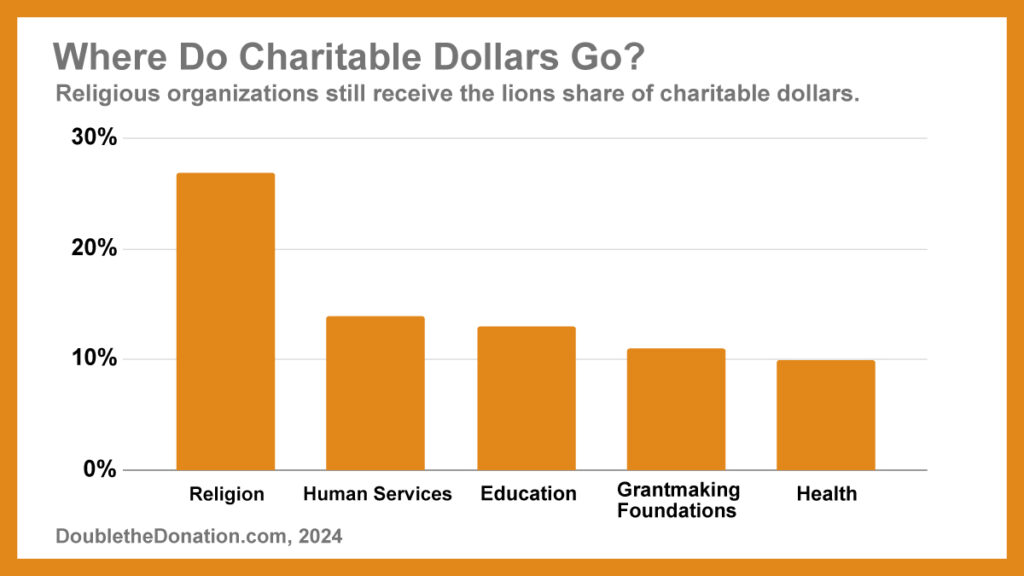

In 2022, the majority of charitable dollars went to religion (27%), human services (14%), education (13%), grantmaking foundations (11%), and health (10%).3

Charitable Giving Strategies

Charitable contributions happen throughout the year, but 30% of all giving occurs in December, with about 10% of all annual donations coming in the last three days of the year. So, if you haven’t yet decided on your giving strategy for 2024, you’re in good company.3

Here are some ideas to consider. After reading the list, be sure to also check out the section called “Key Points to Remember with Charitable Giving Strategies” to learn more about the benefits and limitations of the various approaches.

- Using Your Individual Retirement Account (IRA) to Make Qualified Charitable Distributions: If you are at least 70½ years old, you can donate up to $105,000 from your IRA as a Qualified Charitable Distribution. The distribution may satisfy your annual required minimum distribution (RMD). That way, the RMD won’t be reported on your personal tax return. Current tax law raised the standard deduction, which has influenced some RMD decisions.4

- Donating Appreciated Securities: Suppose you are considering using the proceeds from appreciated securities to make a charitable donation. If that is the case, consider the tax consequences of donating the securities rather than selling the position and donating the cash.4

- Donating Depreciated Securities: Conversely, if you have depreciated securities, you might want to explore the tax consequences of recognizing those losses before making the gift. That approach may allow you to hold the losses, which could be used to offset capital gains in the future.4

- Donor-Advised Funds: Donor-advised funds are registered 501(c)(3) organizations that can be funded with cash, securities, and other assets. Once your donor-advised account is set up, you can decide over time which charities and causes you’d like the funding to go towards. However, donor-advised funds can be restrictive. Because these funds are often sponsored by a community foundation or non-profit (like a hospital or religious organization), there may be restrictions on where and how your grants are used.4

Some donor-advised funds are considered mutual funds and are sold only by prospectus. The prospectus will provide information on charges, risks, expenses, and investment objectives and should be reviewed carefully before investing. Investment companies can provide a prospectus, or you may prefer to ask your financial professional. Please read it carefully before you invest or send money.

- Charitable Remainder Trusts: Charitable remainder trusts are irrevocable trusts that let you donate assets to charity and draw annual income for life or for a specific period. You can transfer property, cash, or other assets into an irrevocable trust. The trust pays income to at least one living beneficiary and continues for a specific term or the life of one or more beneficiaries. At the end of the payment term, the remainder of the trust passes to the charitable organization(s).5

- Charitable Lead Trusts (CLTs): A charitable lead trust (CLT) functions as a “freeze device,” effectively locking in the value of assets transferred into the trust. Any appreciation (or depreciation) in the value of these assets during the trust term occurs within the trust and is excluded from additional gifting or estate considerations upon termination of the trust. The trust makes regular payments to a designated charity for a specified period. After the trust term ends, the remaining assets are distributed to non-charitable beneficiaries, typically family members.6

Key Points to Remember with Charitable Giving Strategies

This blog is for informational purposes only and is not a replacement for real-life advice. Many people want to learn more about the tax pros and cons associated with charitable contributions. We encourage you to speak with your tax, legal, and accounting professionals before making a contribution or implementing a strategy.

Once you reach age 73, you must begin taking RMDs from a traditional IRA in most circumstances. Withdrawals are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty.

With securities, remember that investing involves risks, and investment decisions should be based on your goals, time horizon, and risk tolerance. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost.

Charitable remainder trusts and charitable lead trusts involve a complex set of tax rules and regulations. Before proceeding with either trust, consider working with a professional familiar with the relevant rules and regulations.

Maximizing Your Impact

Charitable giving can be a fulfilling and impactful way to make a difference. As financial professionals, we can help you structure your philanthropy by making it part of your overall financial strategy. We can also have high-level pro and con discussions to help you as you begin the process. Call us, and we can schedule a time to discuss your charitable giving for 2024 and beyond.

1. Giving USA, June 25, 2024 https://cdn.ymaws.com/www.givinginstitute.org/resource/resmgr/gusa/2024_resources/Giving_USA_Press_Release_202.pdf

2. Bank of America Institute, November 10, 2023. https://institute.bankofamerica.com/content/dam/transformation/charitable-affluent-households.pdf

3. Double the Donation, August 2024. https://doublethedonation.com/nonprofit-fundraising-statistics/

4. Nasdaq, March 4, 2024. https://www.nasdaq.com/articles/six-charitable-giving-strategies-for-2024

3. Internal Revenue Service, August 2024. https://www.irs.gov/charities-non-profits/charitable-remainder-trusts

4. The National Law Review, July 19, 2024. https://natlawreview.com/article/rates-decrease-charitable-lead-trusts-will-shine-again